By Captain Riptide — Antigua-born efoil addict, fine-print hunter, and barnacle-scraper of suspicious promises.

Ahoy, mateys! You are standing at the checkout on LiftFoils.com, ready to pull the trigger on a gorgeous new setup. Then the pop-up appears: Lift Protect (powered by SureBright). It promises smooth sailing and total protection against drops, crashes, hard landings, liquid exposure, splashes, and water-related damage to your internal electronics.

It sounds like the ultimate shield. But does the actual contract deliver, or are you buying a paper anchor?

I read the full, binding SureBright Service Contract word for word. I audited Lift’s official warranty policy. No marketing spin. Just the raw, unfiltered truth about how generic insurance language leaves massive, watery loose ends for real efoil riders.

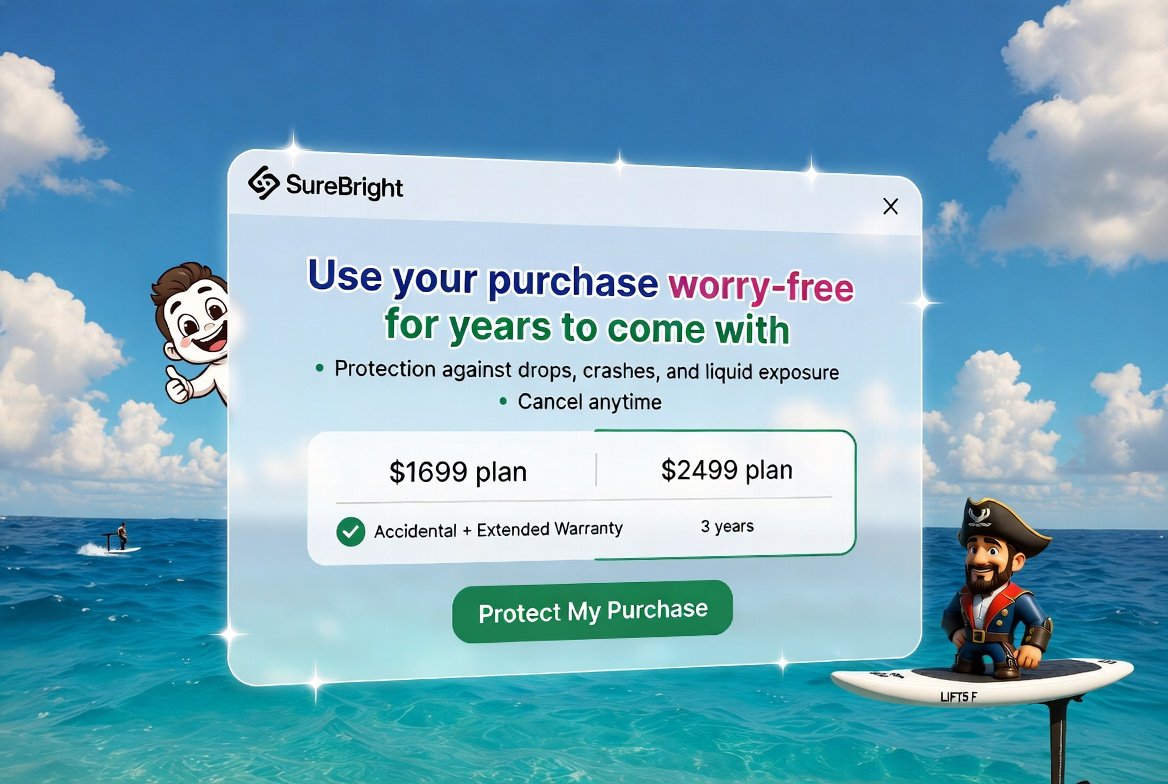

The Four Options at Lift Checkout

Note: Prices are dynamic based on your exact board and cart total. The numbers below reflect premium carbon setups like the LIFT5 Pro or LIFTX lineups. Always verify the math in your own checkout.

| Option | What It Covers | Typical Price Range | Best For |

|---|---|---|---|

| Manufacturer 1-Year Warranty | Defects in materials and workmanship only. | Free(Included) | Everyone as the baseline. |

| Extended Breakdown | Mechanical and electrical failures after year 1. | 2-Year: $199 3-Year: $299 | Post-warranty internal component peace of mind. |

| Accidental Plus Extended | Base breakdown coverage + one (1) ADH claim with a $500 deductible. | 2-Year:$1,699 3-Year:$2,499 | Riders who want a safety net for catastrophic user error. |

| No Thanks | Nothing extra. | $0 | Disciplined self-insurers. |

Export to Sheets

Critical Fine Print Warning: The Immersion Contradiction

The marketing pop-up loudly promises protection against “liquid exposure, splashes, and water-related damage affecting internal electronics.” But if you flip to the actual definitions and exclusions inside the binding SureBright Service Contract, the generic boilerplate creates a massive, conflicting loophole:

“Immersion of Your Covered Product is not covered under this Agreement.”

Let’s unpack how completely absurd that is for an electric hydrofoil. This contract text is generic boilerplate originally written for laptops, cell phones, and blenders. If you drop your iPad into a swimming pool, that is “immersion,” and your warranty is void.

But an efoil lives in the water. It is designed, engineered, and required to be submergeable during normal operation. You can’t take off, execute a deep water start, or navigate a wave without partial or full submersion of major components. By stating that “immersion” is explicitly excluded, the core contract text functionally rules out the very environment the board exists in.

The “Loose Ends” Catch: Accidental vs. Boilerplate

Now, SureBright will argue that if you step up to the expensive Accidental Plus tier, the Accidental Damage from Handling (ADH) rider is meant to cover sudden, unforeseen liquid damage from a riding mishap.

But because they left that massive “immersion” exclusion sitting in the master contract text, it creates a serious legal gray area. The contract fails to define where a covered “accidental water exposure” ends and an excluded “submersion or environmental condition” begins.

If saltwater forces its way past a seal after a hard wipeout, is it covered accidental handling, or will a claims adjuster deny it as an excluded immersion event? It leaves completely loose ends, giving a third-party administrator all the leverage to define your claim based on how you word the incident.

The Cancellation Reality Check

While SureBright is a legitimate digital warranty manager backed by elite startup tech funding (Y Combinator), the actual financial heavy lifting is backed by Universal Underwriters Service Corporation. When you read the deep legal clauses attached to their service contracts, another frustrating operational loose end pops up for owners:

The Pro-Rata Cancellation Penalty

If you buy a 3-year contract, have an electrical issue fixed in month 14 that costs $800, and later decide to sell your efoil and cancel the remainder of the warranty for a partial refund, SureBright subtracts the cost of that repair from your refund check in most states. You are essentially penalized for actually using the product you paid for.

Value Analysis: Why the Max Coverage Is Rarely Worth It

On a typical premium Lift setup, the Accidental Plus Extended plan costs between 11% and 17% of the entire board’s retail price. That is a massive upfront premium.

Beyond the misleading water language, here is why the math simply doesn’t track:

The Single-Bullet Constraint: The contract grants you exactly one (1) ADH (Accidental Damage from Handling) claim for the entire multi-year term. Once you use it, your accidental coverage is completely exhausted.

Let’s look at the actual replacement parts catalog for a Lift Foils rig:

- Full-Range Lithium Battery: ~$3,950

- Replacement Carbon Mast (excluding motor assembly): $1,499 – $1,920

- Fixed Aluminum Propeller: $390

- Folding Propeller Kit: $250

The Verdant Ride Math Example

Let’s say you buy the 3-Year Accidental Plus plan for $2,499.

In your second month of riding, you misjudge a reef and suffer a catastrophic impact that cracks your battery casing, causing immediate water ingress.

- You pay your $2,499 upfront premium.

- You file your single allowed ADH claim and pay the mandatory $500 deductible.

- Your total out-of-pocket cost for this single resolution is $2,999.

Given that a brand-new, full-range battery retails for $3,950, you only saved about $951—and your accidental protection is now totally gone for the remaining 34 months of your policy. If you hit a sandbar or drop your mast next summer, you are entirely on your own.

Captain Riptide’s Final Verdict

SureBright is a legitimate company, but their contract terms are written for a smartphone, not a high-performance personal watercraft. If you want protection against clean, internal electrical or mechanical failures after the factory warranty expires, the Base Extended Warranty ($199–$299) is a reasonable value.

However, the Accidental Plus Max Coverage ($1,699–$2,499) contains way too many contradictory loose ends regarding water damage to justify the massive upfront price tag.

Verdant Ride Recommendations

- Pass on the Accidental Pop-Up: You are better off self-insuring. Take that $2,500 premium, park it in a dedicated high-yield savings account as your personal “repair fund,” and practice obsessive rinsing, drying, and maintenance.

- The Real Insurance Alternative: Call a specialty marine insurance broker and look into custom personal watercraft policies from outfits like XINSURANCE or RecProtect, which actually understand what submergeable hardware means.

Broker Warning: Do not rely on your standard Homeowners or Renters insurance policy. Because an efoil is motorized and houses a massive lithium-ion battery, standard homeowners underwriting guidelines almost universally exclude them, classifying them strictly as Personal Watercraft (PWC).

Fair winds, clear seals, dry electronics, and well-documented claims, hearties!

Full Sources (All Verifiable as of May 2026)

- SureBright Master Service Contract / Detailed Terms and ConditionsSource Document: Direct customer link shown at Lift Checkout / Active Policy PDF ID:

uploaded:SureBright - Customer Portal.pdf* Verifies the specific boilerplate exclusion: “Immersion of Your Covered Product is not covered under this Agreement.” * Verifies the strict “one ADH claim limit” rule per multi-year contract term.- Verifies that the designated ultimate underwriting entity (Obligor) is Universal Underwriters Service Corporation, headquartered at 7045 College Boulevard, Overland Park, KS 66211.

- SureBright State-Specific Amendments Policy Clauses Source Document: State Endorsement Appendix (

uploaded:SureBright - Customer Portal.pdf, p. 1, 9) * Verifies the pro-rata cancellation policy where the cost of any past repairs performed under the warranty is legally deducted from the customer’s remaining premium refund balance upon cancellation. - Lift Foils Official Limited Warranty Page Link: https://liftfoils.com/pages/warranty (Accessed May 2026) * Verifies the parameters of the baseline 1-Year Manufacturer Warranty, including the explicit exclusion of water intrusion due to user error, crash impacts, or environmental corrosion, alongside non-transferability parameters.

- Live Lift Protect Checkout Modal & Pricing Tiers Link: https://liftfoils.com (Observed Checkout Data for LIFT5 Pro and LIFTX Series configurations) * Verifies the dynamic pricing structure separating the Base Extended Breakdown tiers ($199–$299) from the high-tier Accidental Plus Extended tiers ($1,699–$2,499).

- Lift Foils Component & Replacement Hardware Retail Pricing Link: LiftFoils.com Official Parts Store (Current Catalog Matrix as of May 2026) * Verifies market replacement metrics used in value analysis formulas: Full-Range Lithium Battery (~$3,950), Replacement Carbon Masts ($1,499–$1,920), and Propulsion/Propeller Kits ($250–$390).

- Y Combinator Company Database & Insurtech Startup Profiles Link: https://www.ycombinator.com/companies/surebright (Summer 2024 Batch Listings) * Verifies SureBright’s background as a legitimate, platform-backed digital warranty software platform servicing embedded e-commerce merchants.

- Shopify App Store Developer Profiles & Merchant Feedback Matrix Link: https://apps.shopify.com/surebright* Verifies active merchant platform implementation status and historical review aggregations (averaging a 4.7–5.0 star metric).

- Alternative Specialized Marine Watercraft & High-Risk Action Sports Coverage Guides Links: RecProtect Specialty Watercraft Lines (https://recprotect.com) & XINSURANCE High-Risk Marine Operations (https://xinsurance.com) * Verifies existence of specialized operational hulls, liability, and physical hull damage policies written specifically for motorized, lithium-ion personal watercraft (PWC) as alternatives to generic consumer electronics protection plans.

Leave a Reply